With the emerging success and adoption of standardised APIs, data analytics and widespread collaboration, it seems to be a good time to be in fintech. Is the hype overblown, or are these trends set to continue? Patrick Brusnahan reports

Open Banking has spurred a multitude of innovation, according to the World Fintech Report 2019, written by Capgemini and Efma.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The report states that the financial sector is moving to a phase it calls “Open X”.

It states: “Open X will allow the industry to leapfrog Open Banking principles and foster a seamless exchange of resources, improved experience for customers, and expedited product innovation.

“And although today’s incumbent banks may not be perfectly suited to orchestrate this Open X ecosystem, they can profitably succeed in new roles.”

What is Open X?

Open X concerns itself with four fundamental shifts in the sector:

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalData- A move away from products to an emphasis on customer experience;

- Less emphasis on assets and more on data;

- Shared access instead of ownership, and

- Partnering rather than buying or building.

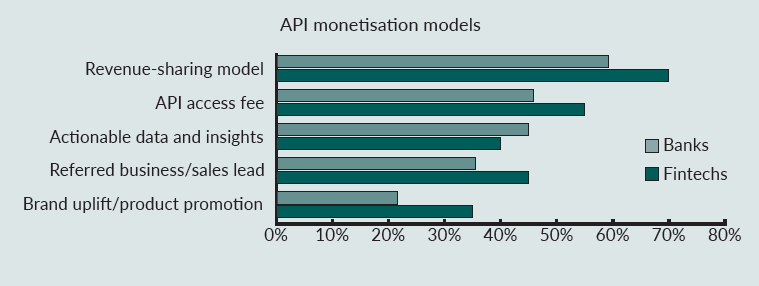

What will link all these factors is the open API. Those that lead API standardisation initiatives and look for real monetisation value with indirect models are set to get the most out of the endeavour.

The biggest shift is that if Open X comes into play, banks will not necessarily own the overall customer experience in the new ecosystem; they will need to integrate with other players. On the other hand, fintechs do not typically have the size and scale of operation required, so collaboration with banks looks to be a way forward.

The report states that this model could “surmount concerns and obstacles around open architecture adoption and implementation”.

“Open Banking has long been regarded as transformational for financial services, but this report shows it is just one part of a much bigger picture,” says Anirban Bose, CEO of Capgemini’s financial services unit and member of its group executive board.

“The industry is on the verge of a more comprehensive evolution, where there is opportunity to leapfrog into an integrated marketplace that we are calling Open X.

“In Open X, there will be seamless sharing of data, and ecosystem partners will be able to collaborate in a far more comprehensive way. Our research suggests that banks and fintechs need to prepare themselves for a more radical change than many previously anticipated.”

“The findings of the report could not be clearer: collaboration will be the foundation of the future of financial services,” adds Efma secretary general Vincent Bastid.

“In the era of Open X, ecosystem players will have to work together more effectively than they have previously. Only by embracing collaboration and new, specialist roles can both banks and fintechs thrive and best serve their customers.

“It’s clear that many barriers to collaboration still exist, and there is an urgent need to overcome them for collective benefit.”

![]()

The Open ecosystem

The report states: “The open ecosystem of the future will feature emergent new roles that challenge traditional banking assumptions.”

Capgemini and Efma describe three roles in the new ecosystem: supplier, aggregator and orchestrator. If Open X becomes a reality, established banks may not be suited for the orchestrator role; they will have to leverage their capabilities to add value as suppliers and aggregators.

Banks need to prioritise the enhancement the robustness of their internal integrated model. Using data and technology, as well as available expertise, incumbents can modernise and optimise internal processes. This can enable competitive delivery of relevant services.

While Open Banking is still an emerging concept, it is at risk of being outdated before it has fully arrived. Open X, it would appear, is the next phase. Open X will be a shared marketplace in which “players leverage data extensively and collaborate with other players to provide customers with a seamless experience”.

A key condition is that banks will need to integrate within the whole customer journey. In addition, this must happen whether banks control the whole process or not.

Banks are agreeing that fintechs are beneficial to the industry. The report quotes Siew Choo Soh, head of consumer banking and big data/AI technology at DBS, saying: “Participation from fintechs and rising customer expectations are some of the best things that have happened in the financial industry. They force incumbents to leave their comfort zone, change their business model, culture, and technology architecture, to trigger a digital transformation tsunami.”

Laurent Darmen, CEO of La Fabrique by Crédit Agricole, says: “The traditional bank must progressively move from a position of ‘universal bank’ to a position of ‘universal partner’ to support customers beyond strictly banking products. Indeed, financial services are at the crossroads of customer journeys. This is an orientation towards a more useful but less visible bank.”

“Transformation or re-engineering often takes time,” states Tara Welkley, head of Open Banking at Citi Fintech. “Partnering with a fintech should accelerate the delivery schedule of a new solution, allow for a pivot if a new opportunity emerges, and/or if consumer preferences change.

“Fintechs and other service providers are able to supplement banks’ core offerings and enrich traditional products.”